Contact Us

Subscribe to Causeway Insights, delivered to your inbox.

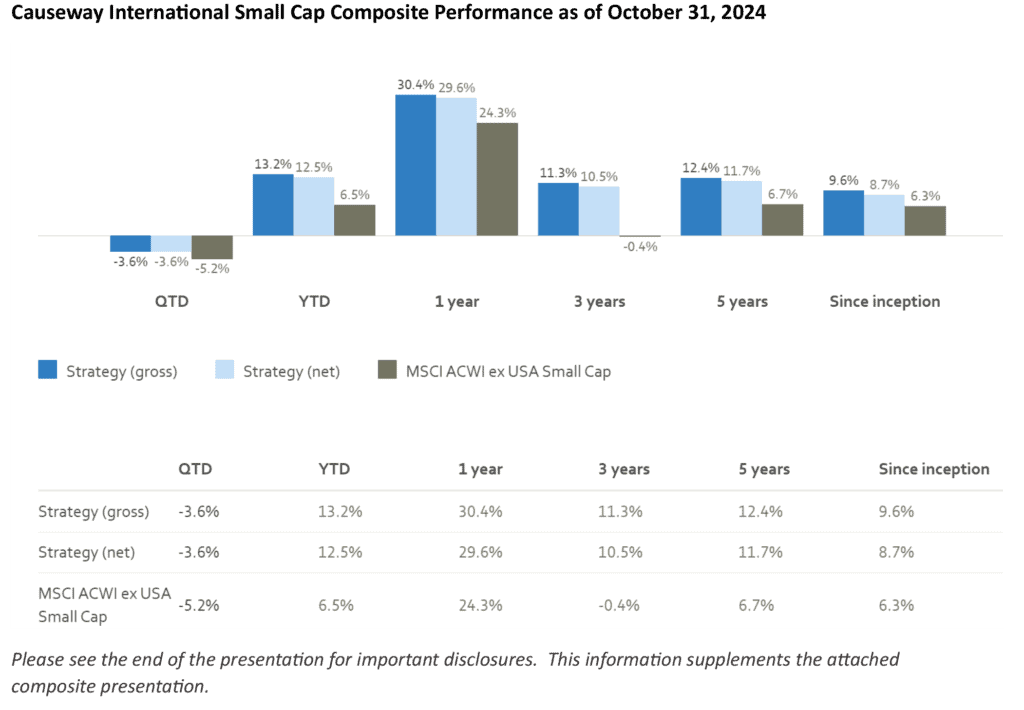

November marks a decade of managing Causeway’s International Small Cap (ISC) equity strategy. Since its inception, our ISC composite has outperformed the MSCI ACWI ex-USA Small Cap Index across all standard time frames. This milestone is a testament to the proficiency of our quantitative portfolio managers, who have honed their skills in international small caps, applying rigorous multi-factor modeling to identify unique opportunities in this diverse and dynamic asset class.

To mark this achievement, Causeway quantitative portfolio managers joined senior relationship manager Sarah Van Ness to discuss the unique attributes that make international small caps compelling and to share quantitative and fundamental insights that have shaped our approach to this asset class.

Listen to our audio interview or read on for their comments.

Key insights

- International small caps offer exposure to under-owned stocks in great breadth, providing domestic economic exposure that larger-cap stocks often lack.

- Small caps tend to have low correlations, allowing for diversified portfolios with volatility comparable to mid- and large-cap portfolios.

- Causeway’s multi-factor model includes natural language processing and network momentum factors to seek to identify and capitalize on small cap inefficiencies.

First off, congratulations on the track record. Let’s begin broadly, with the asset class: tell me about the investable universe for international small caps.

Duff Kuhnert: There is tremendous breadth—more than 4,000 small cap stocks listed in 46 developed and emerging equity markets spanning every industry, including approximately 3,300 that currently meet our trading liquidity requirements. There are so many fish in the small cap sea. It’s easier to build portfolios that are attractive on multiple dimensions—value, growth, momentum, quality—when you have this much choice. At Causeway, we focus on stocks that are in the top 5% when considering those dimensions together. With an investable universe that large, you can get a portfolio that’s really well diversified at 120-200 stocks and looks attractive on a range of characteristics.

Ryan Myers: And international small caps are often massively under-owned. They comprise over 5% of the float of the MSCI ACWI IMI index as of October 31, and 50% the number of stocks. But according to Morningstar, US mutual funds, in aggregate, allocate less than 1% of their public equity investments to international small cap companies. That is less than 1% allocated to more than half the stocks in the world.

Arjun Jayaraman: It is a domestically focused asset class, in terms of economic exposure. You will typically get more “true” country exposure by investing in small caps than in large caps, where multinationals are a big presence.

What are some of the most attractive features of small caps?

Arjun: An ideal feature, for quants especially, is that small cap benchmarks don’t get these massive distortions from large cap stocks. If a small cap company does well, it gets promoted to a larger-cap index. So, the concentration risk tends to be limited.

You also don’t have the level of country concentration that you have in large cap benchmarks. Small caps haven’t had the seismic changes we’ve seen in the large cap space, like the dominance of the US. By nature, it has been more stable index construction: very flat and well distributed, which we think is perfect for quantitative strategies.

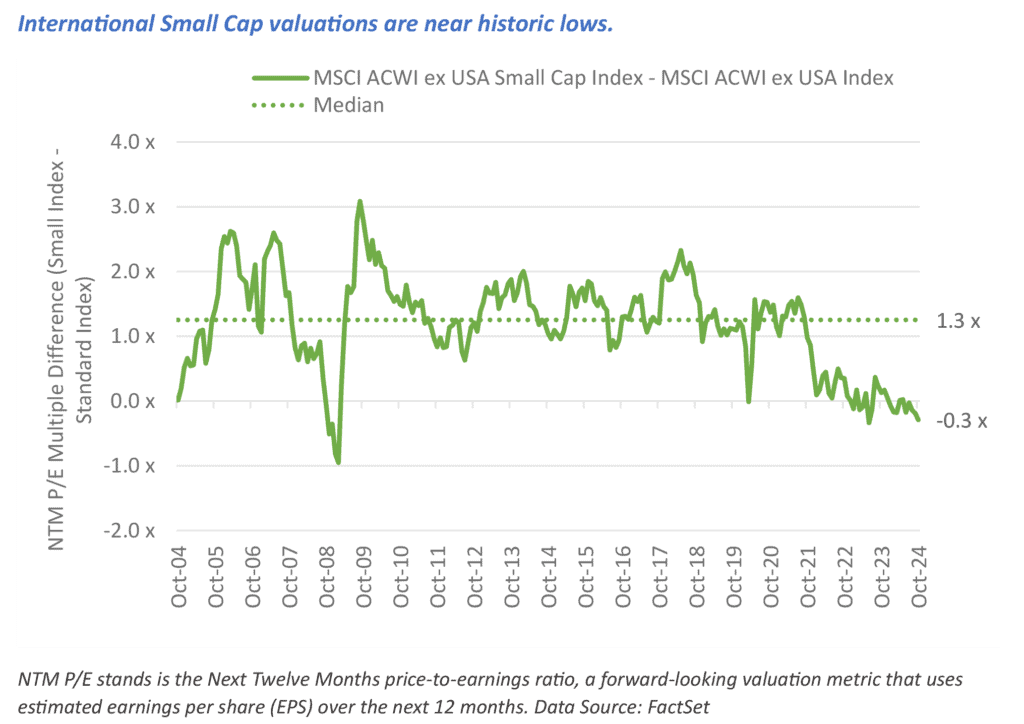

Ryan: I’d say the valuation disconnect, although it may not persist much longer. It’s reaching a historic discount, relative to both large caps and its own history. You can’t say that about any other part of the global equity landscape.

Duff: I like the limits on arbitrage, like high borrow costs for shorting. When there’s mispricing in large cap US companies, money swoops in very quickly to arbitrage that mispricing. But in international small cap, because of the higher borrow costs and because of the higher volatility at the stock level, arbitrage is not easy. Mispricing persists, and strategies like ours can seek to take advantage of it.

Joe Gubler: Yes, investing strategies that tend to enforce more efficiency on certain parts of the market are harder to implement here, like leveraged long/short. Plus, fewer investors—as Ryan said, people are typically under-allocated—have kept the market inefficient.

How about common small cap misconceptions?

Duff: I think people overestimate their risk. Yes, the volatility of individual small cap stocks is typically higher compared to larger caps, but what investors may not appreciate is the low correlation between small cap stocks. For example, two of the largest-weighted positions in our current international small cap portfolio are a Taiwanese technology company and an Italian insurer. Those two stocks operate in different contexts and have very little in common. Their correlation is actually negative.

Joe: It’s such a diverse opportunity set with stocks that tend to move independently. If you put them all together in a risk-conscious way, you can largely achieve portfolio volatility as low as a large cap developed index.

Ryan: And to mitigate individual stock volatility, we use our quality factors, which include measures of both competitive and financial strength. Quality is very important for small caps, which can have a higher failure rate and higher individual volatility. A comprehensive risk model and our fundamental review process add more risk mitigants.

How has the asset class changed over the past decade?

Duff: India has really blossomed in terms of investment, both in terms of liquidity and trading volume. There are a lot more stocks that meet our average daily trading volume requirements. China really doesn’t play much of a role anymore. Over the past ten years, due to underperformance and changes to MSCI index construction methodology, China went from the largest emerging market weight in international small caps to the fourth largest, currently less than 3% of the MSCI ACWI ex-USA Small Cap Index. Over that same period, India’s index weight has grown from below 2% to over 9%, the second-largest small cap market by weight, across developed and emerging, in the asset class.

Arjun: US and India are two major stock markets globally that have performed well over the past two years, but they’ve generally been mirror images of each other. The US has been driven by dominant mega-caps, while the emergence of India is about small caps. We believe it’s a small cap story because India’s gross domestic product is growing 6-7% per year, and small caps offer the most direct exposure to that growth.

And Causeway’s International Small Cap strategy—how has it evolved?

Arjun: One key evolution for Causeway small cap—for all Causeway quant-driven strategies—is to expand beyond the four-factor food group approach. We have value, growth, quality, and technical, then this year we’ve added uncorrelated, differentiated factors, like a corporate events factor category.

Joe: We have tailored our alpha models. If we have an alpha model that generally works well but has certain types of stocks where we believe it can do better, we ask, what can we do about that? For example, this year we adjusted our earnings growth factors to account for commodity spot prices for stocks sensitive to those movements.

Duff: One of the most influential enhancements we made was implementing a network momentum factor in 2021, which recognizes that positive (or negative) information for one stock can flow through to the performance of related companies, like competitors, customers, industry peers, and companies that discuss similar topics during their conference calls. Japan is the largest country in international small cap, and standard momentum factors haven’t generally worked well. But network momentum has. Identifying a technical factor that works in this important small cap market has been beneficial.

Ryan: We’ve added earnings and guidance announcement return factors. We’ve added additional quality factors. We’ve added natural language processing (NLP). With all these different sources of alpha working together we have a model that has been able to generate a consistent return stream.

We launched a Global Small Cap strategy in 2023. Are there plans to expand Causeway’s small cap strategies further?

Arjun: Global Small Cap extends Causeway’s reach to include US small caps alongside international stocks. We developed a distinct alpha model for the US. Thanks to our quant approach, we believe we can customize market exposure based on client needs—whether that’s developed-markets-only or another adaptation.

Many Causeway clients are asking about artificial intelligence (AI) opportunities—not only for portfolio holdings, but also for our investment processes. Can you share some examples?

Joe: We’re really focused on what can we do with AI and natural language processing (NLP) and machine learning. Like using NLP on company transcripts to identify peer groups for our network momentum factor. The recent AI boom has created strange bedfellows. For example, an HVAC company in the US that makes ventilation and air conditioning systems. Our NLP analysis identifies them as a network peer of major AI stocks because they’re cooling the data centers. It wasn’t a peer in the past. It may not be in the future. But NLP can try to identify and exploit current relationships like that.

Ryan: We also are using NLP to get sentiment from earnings transcripts. This could be especially useful in small caps, which often are not well-covered by sell-side research. NLP can tell you a lot about sentiment from these transcripts.

Arjun: As computing power increases—and as firms can lease this power via the cloud—these approaches are more reasonable than they were, say, five or ten years ago. It’s leveled the playing field between us and the big quant firms in terms of computing power. And then, of course, if you think about Causeway and our fundamental capabilities, we have something that is not easily replicated.

You brought up fundamental research. Clients also ask, how does Causeway’s fundamental capability contribute to a quant-driven small cap strategy?

Arjun: It’s interesting to see the different ways in which fundamental investors and quant investors think about the world. Quants love to extrapolate from the past and say it’s going to continue. But that’s not how our fundamental analysts think, especially in terms of cyclical industries. For cyclicals, they think about peak and trough margins. We are currently researching a factor for cyclical companies inspired by their approach.

Duff: We get important stock-level feedback from our fundamental colleagues. We meet with them monthly to go through larger-weight positions within every sector with the relevant sector specialists.

Ryan: Small caps tend to be concentrated in their businesses, which can create more risk than a larger, diversified company. Our real estate analysts have identified companies that are overly concentrated in specific regions. And our fundamental analysts are often knowledgeable about small cap companies as competitors or suppliers of companies in their direct coverage, even if the company is not investable for our other strategies that tend to focus on larger cap companies. For example, our health care analysts track new drug development, often occurring at small firms. They have given us helpful feedback on our small cap trades.

Having a multi-factor model, particularly one that emphasizes value factors, came under scrutiny in what we call at Causeway the “value winter,” from 2019 to 2021. Does value have a place in small-cap?

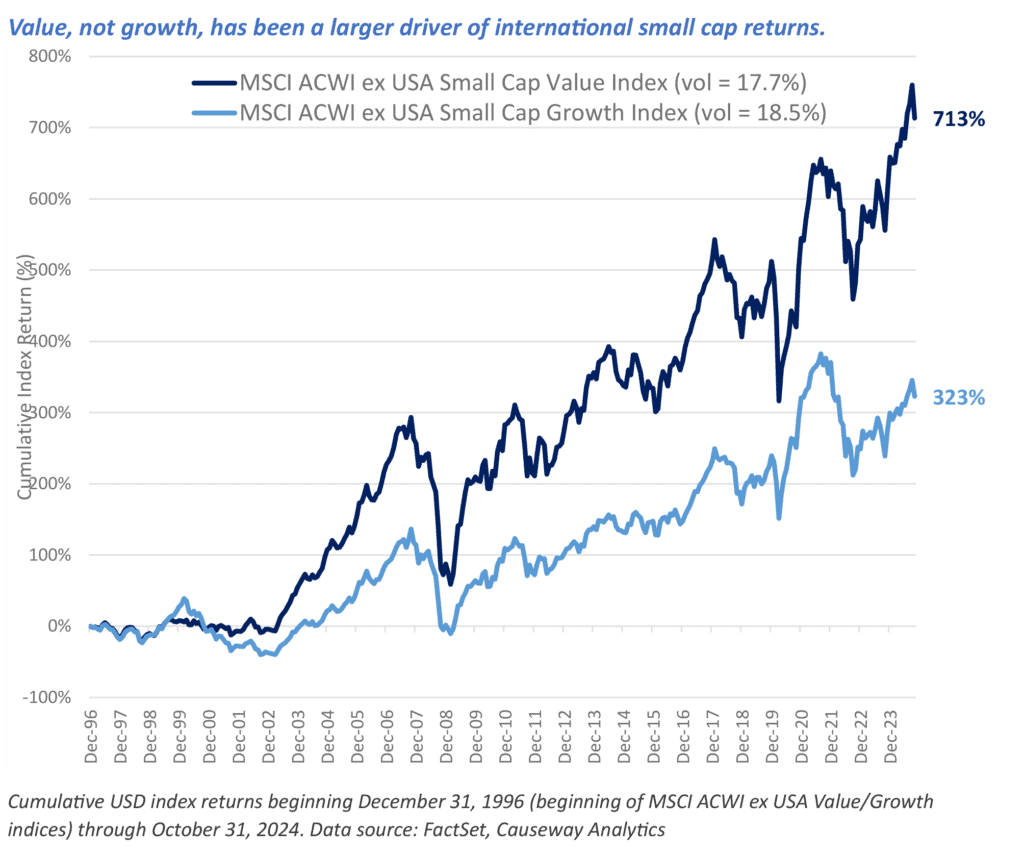

Ryan: People don’t associate small caps with value, but value has historically outperformed growth in international small caps. It is an important driver of returns.

Arjun: Through the pandemic, there was a general feeling that value is dead, and we did have pressure from various constituents to get more “growthy.” We pushed back on that and stuck to our multifactor discipline— and we believe our clients have been rewarded as the subsequent three years achieved strong performance. The worst thing in the world is to change what you’re doing based on temporary environments.

Joe: Many investors barely reach the threshold of making a dedicated small cap allocation, and when they do, they often allocate to one manager. Our goal has been to create a strategy that’s diversified from an alpha perspective and carefully managed from a risk perspective. And if you look at our relative performance over time, it has not relied on a particular style being in favor.

Ryan: This process is thorough, scoring every stock in our investable universe every day along multiple alpha factors. We designed the strategy with a philosophy to leave no stone unturned.

What’s on the horizon for small caps and Causeway’s small cap strategies?

Arjun: We are enthusiastic about the next decade. As we’ve discussed, the small-cap landscape offers a compelling blend of undervaluation and untapped potential, particularly in rapidly growing markets like India. Our commitment to leveraging advanced quantitative techniques—including AI, NLP, and alternative data—plus insights from our fundamental team, should position us well. Our multi-factor approach has demonstrated its resilience, and with tailored enhancements for key markets, we’re confident that our strategy will continue to unlock opportunities for our clients in the years to come.

This article has been edited for clarity.

This market commentary expresses Causeway’s views as of November 2024 and should not be relied on as research or investment advice regarding any stock. These views and any portfolio holdings and characteristics are subject to change. There is no guarantee that any forecasts made will come to pass. Forecasts are subject to numerous assumptions, risks, and uncertainties, which change over time, and Causeway undertakes no duty to update any such forecasts. Information and data presented has been developed internally and/or obtained from sources believed to be reliable; however, Causeway does not guarantee the accuracy, adequacy, or completeness of such information.

The views herein represent an assessment of companies at a specific time and are subject to change. There is no guarantee that any forecast made will come to pass. This information should not be relied on as investment advice and is not a recommendation to buy or sell any security. The securities identified and described do not represent all of the securities purchased, sold, or recommended for client accounts. Our investment portfolios may or may not hold the securities mentioned. The reader should not assume that an investment in the securities identified was or will be profitable. For full performance information regarding Causeway’s strategies, please see www.causewaycap.com.

The MSCI ACWI ex-US Small Cap Index captures small cap representation across 22 of 23 Developed Markets countries (excluding the US) and 24 Emerging Markets countries. The MSCI ACWI Investable Market Index (IMI) captures large, mid and small cap representation across 23 Developed Markets and 24 Emerging Markets. The MSCI ACWI ex USA Index captures large and mid cap representation across 22 of 23 Developed Markets countries (excluding the US) and 24 Emerging Markets countries. The MSCI Emerging Markets Index captures large and mid cap representation across 24 Emerging Markets countries. With 1,277 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country. The MSCI USA Index is designed to measure the performance of the large and mid cap segments of the US market. The MSCI EAFE Index is an equity index which captures large and mid cap representation across 21 Developed Markets countries around the world, excluding the US and Canada. The MSCI ACWI ex USA Small Cap Value Index captures small cap securities exhibiting overall value style characteristics across 22 of 23 Developed Markets countries (excluding the US) and 24 Emerging Markets countries. The value investment style characteristics for index construction are defined using three variables: book value to price, 12-month forward earnings to price and dividend yield. The MSCI ACWI ex USA Small Cap Growth Index captures small cap securities exhibiting overall growth style characteristics across 22 of 23 Developed Markets countries (excluding the US) and 24 Emerging Markets countries. The growth investment style characteristics for index construction are defined using five variables: long-term forward EPS growth rate, short-term forward EPS growth rate, current internal growth rate and long-term historical EPS growth trend and long-term historical sales per share growth trend It is not possible to invest directly in an index.

MSCI has not approved, reviewed, or produced this report, makes no express or implied warranties or representations and is not liable whatsoever for any data in the report. You may not redistribute the MSCI data or use it as a basis for other indices or investment products.

Notes:

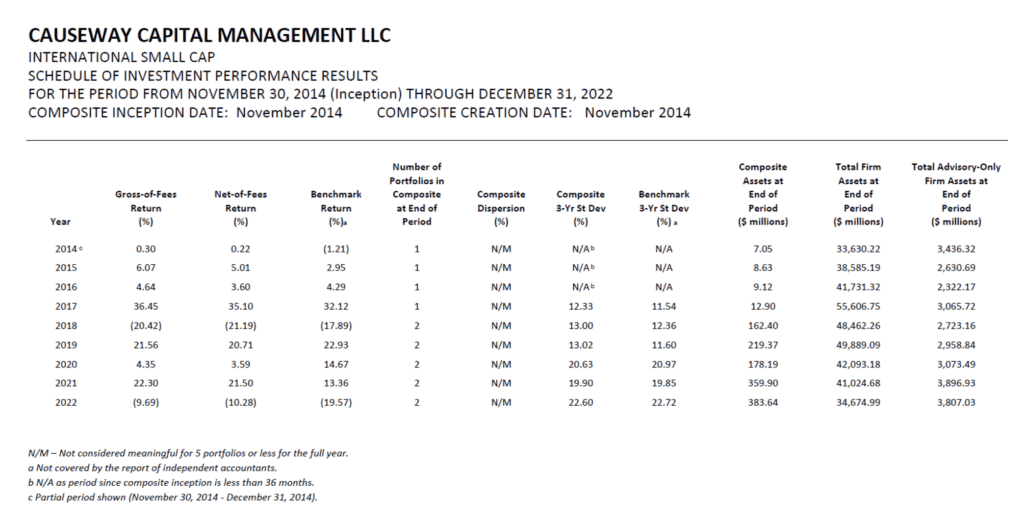

Causeway Capital Management LLC (Causeway) claims compliance with the Global Investment Performance Standards (GIPS®) and has prepared and presented this report in compliance with the GIPS standards. Causeway has been independently verified for the periods June 11, 2001 through December 31, 2022.

A firm that claims compliance with the GIPS standards must establish policies and procedures for complying with all the applicable requirements of the GIPS standards. Verification provides assurance on whether the firm’s policies and procedures related to composite and pooled fund maintenance, as well as the calculation, presentation, and distribution of performance, have been designed in compliance with the GIPS standards and have been implemented on a firm-wide basis. The International Small Cap Composite has had a performance examination for the periods November 30, 2014 through December 31, 2022. The verification and performance examination reports are available upon request. GIPS® is a registered trademark of CFA Institute. CFA Institute does not endorse or promote this organization, nor does it warrant the accuracy or quality of the content contained herein.

The Firm, Causeway, is organized as a Delaware limited liability company and began operations in June 2001. It is registered as an investment adviser with the U.S. Securities and Exchange Commission under the Investment Advisers Act of 1940. Registration does not imply a certain level of skill or training. Causeway manages international, global, and emerging markets equity assets primarily for institutional clients including corporations, pension plans, sovereign wealth funds, superannuation funds, public retirement plans, Taft-Hartley pension plans, endowments and foundations, mutual funds and other collective investment vehicles, charities, private trusts and funds, model and SMA programs, and other institutions. The Firm includes all discretionary and non-discretionary accounts managed by Causeway.

The International Small Cap Composite includes all U.S. dollar denominated, discretionary accounts in the international small cap equity strategy. The international small cap equity strategy seeks long-term growth of capital through investment primarily in common stocks of companies with small market capitalizations located in developed and emerging markets outside the U.S using a quantitative investment approach. New accounts are included in the International Small Cap Composite during the first full . Terminated accounts are included in the International Small Cap Composite through the last full month under management. A complete list and description of Firm composites is available upon request.

Account returns are calculated daily. Monthly account returns are calculated by geometrically linking the daily returns. The return of the International Small Cap Composite is calculated monthly by weighting monthly account returns by the beginning market values. Valuations and returns are computed and stated in U.S. dollars. Returns include the reinvestment of interest, dividends and any capital gains. Returns are calculated gross of withholding taxes on dividends, interest income, and capital gains. The Firm’s policies for valuing portfolios, calculating performance, and preparing compliant presentations are available upon request. Past performance is no guarantee of future performance. Composite dispersion, if applicable, is calculated using the equal-weighted standard deviation of all portfolios that were included in the International Small Cap Composite for the entire year. The three-year annualized ex-post standard deviation quantifies the variability of the composite or benchmark returns over the preceding 36-month period.

The benchmark of the International Small Cap Composite is the MSCI ACWI ex USA Small Cap Index, which is a free float-adjusted market capitalization weighted index, designed to measure the equity market performance of smaller capitalization stocks in developed and emerging markets excluding the U.S. market, consisting of 46 country indices. The Index covers approximately 14% of the free float-adjusted market capitalization in each country. The Index is gross of withholding taxes, assumes reinvestment of dividends and capital gains, and assumes no management, custody, transaction or other expenses. Accounts in the International Small Cap Composite may invest in countries not included in the MSCI ACWI ex USA Small Cap Index, and may use different benchmarks.

Gross-of-fees returns are presented before management, performance and custody fees but after trading expenses. Net-of-fees returns are presented after the deduction of actual management fees, performance-based fees, and all trading expenses, but before custody fees. Causeway’s basic management fee schedules are described in its Firm brochure pursuant to Part 2 of Form ADV. The basic separate account annual fee schedule for international small cap equity assets under management is: 0.80% of the first $150 million and 0.65% thereafter. Accounts in the International Small Cap Composite may have different fee schedules.

MSCI has not approved, reviewed or produced this report, makes no express or implied warranties or representations, and is not liable whatsoever for any data in the report. You may not redistribute the MSCI data or use it as a basis for other indices or investment products.