Contact Us

Subscribe to Causeway Insights, delivered to your inbox.

Smaller, less researched stocks can offer valuation discounts and more growth potential than their larger capitalization peers. But what is the most effective method to exploit those pricing inefficiencies? We introduce Causeway International Small Cap Fund, and explore how we combine the flexibility and breadth of quantitative research with fundamental industry knowledge, to access lucrative opportunities in developed and emerging markets small cap stocks.

As Mark Twain once said, “It’s not the size of the dog in the fight, it’s the size of the fight in the dog.” We recognize that smaller, less- researched stocks can offer valuation discounts and more growth potential than their larger capitalization peers. But what is the most effective method to exploit those pricing inefficiencies? Quantitative research and portfolio construction typically have flexibility in investment style and the agility to react to upside opportunities. Combine that quantitative rigor with fundamental industry knowledge, and the result can exceed what either investment approach could do in isolation.

With both developed and emerging markets in the MSCI ACWI ex USA Small Cap Index (“ACWI ex-US Small Cap Index”) as our hunting grounds, we have launched the Causeway International Small Cap Fund. To learn more about the Fund, we spoke to Causeway portfolio managers Arjun Jayaraman, Duff Kuhnert, and Joe Gubler, the architects of Causeway’s International Small Cap strategy.

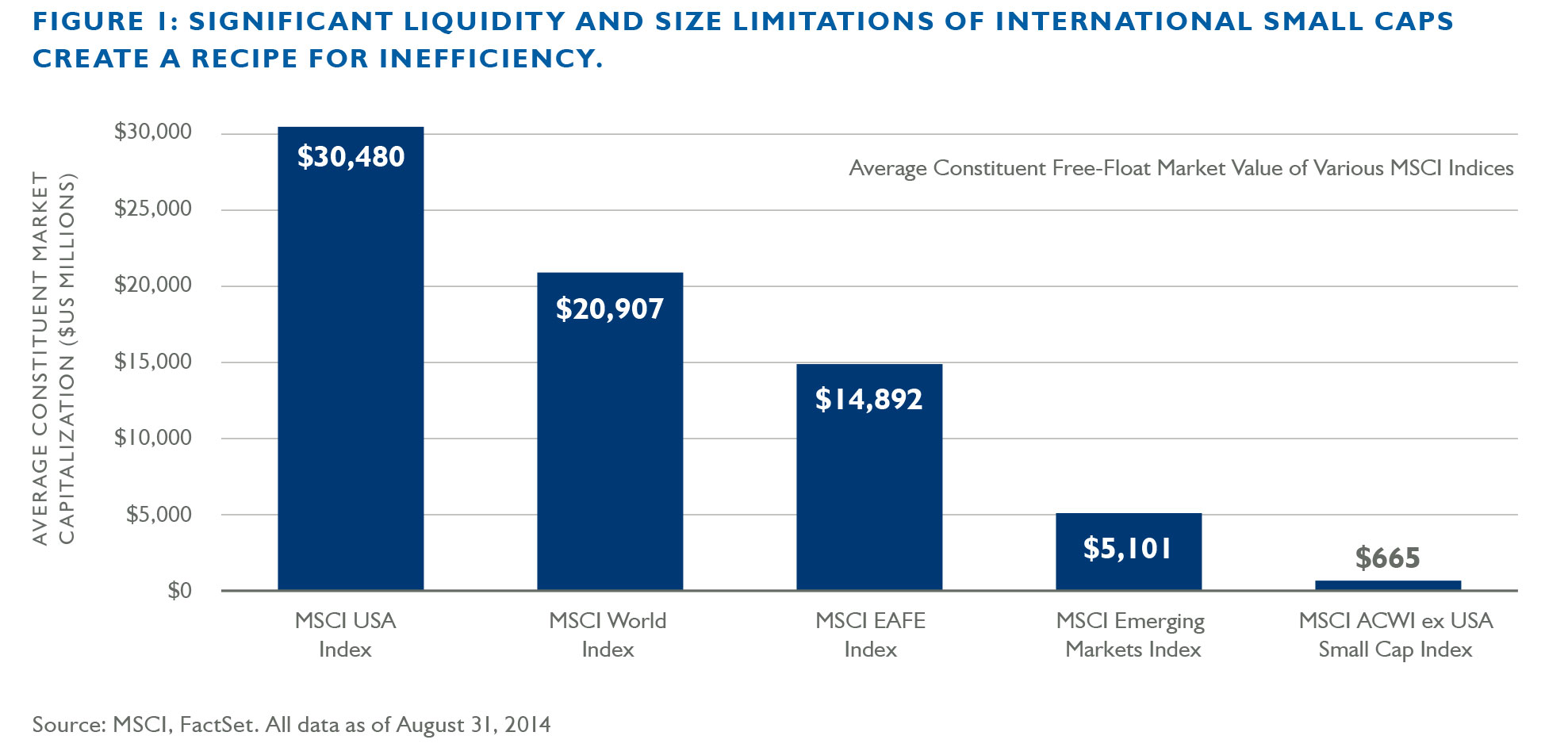

We believe that the intersection of international equities and smaller capitalization companies creates a recipe for inefficiency.

Arjun, what makes international small-cap equities attractive?

AJ: We believe that the intersection of international equities and smaller capitalization companies creates a recipe for inefficiency. Many international stocks – especially those in emerging markets – have less sell-side research coverage than their U.S. peers, and their share prices often do not fully reflect publicly available information. The relatively lower liquidity of international small cap companies also discourages research coverage, prolongs information dissemination, and expands pricing inefficiencies. For instance, the average free float market value of the ACWI ex-US Small Cap Index was U.S. $665 million as of August 31, 2014. These smaller stocks require an equivalent research effort to their larger brethren. Yet, with liquidity and size limitations, many stocks with market capitalizations under $1 billion just are not worth the effort for many larger funds because their average position size would overwhelm available daily trading volumes. Additionally, many emerging markets impose regulatory hurdles to short selling. Coupled with increased borrowing difficulties, these hurdles largely silence the perspective of short sellers in those markets. The net result is that investors often ignore many non-US small cap equities, making them fertile ground for stock selection for those able and nimble enough to take advantage of the opportunity.

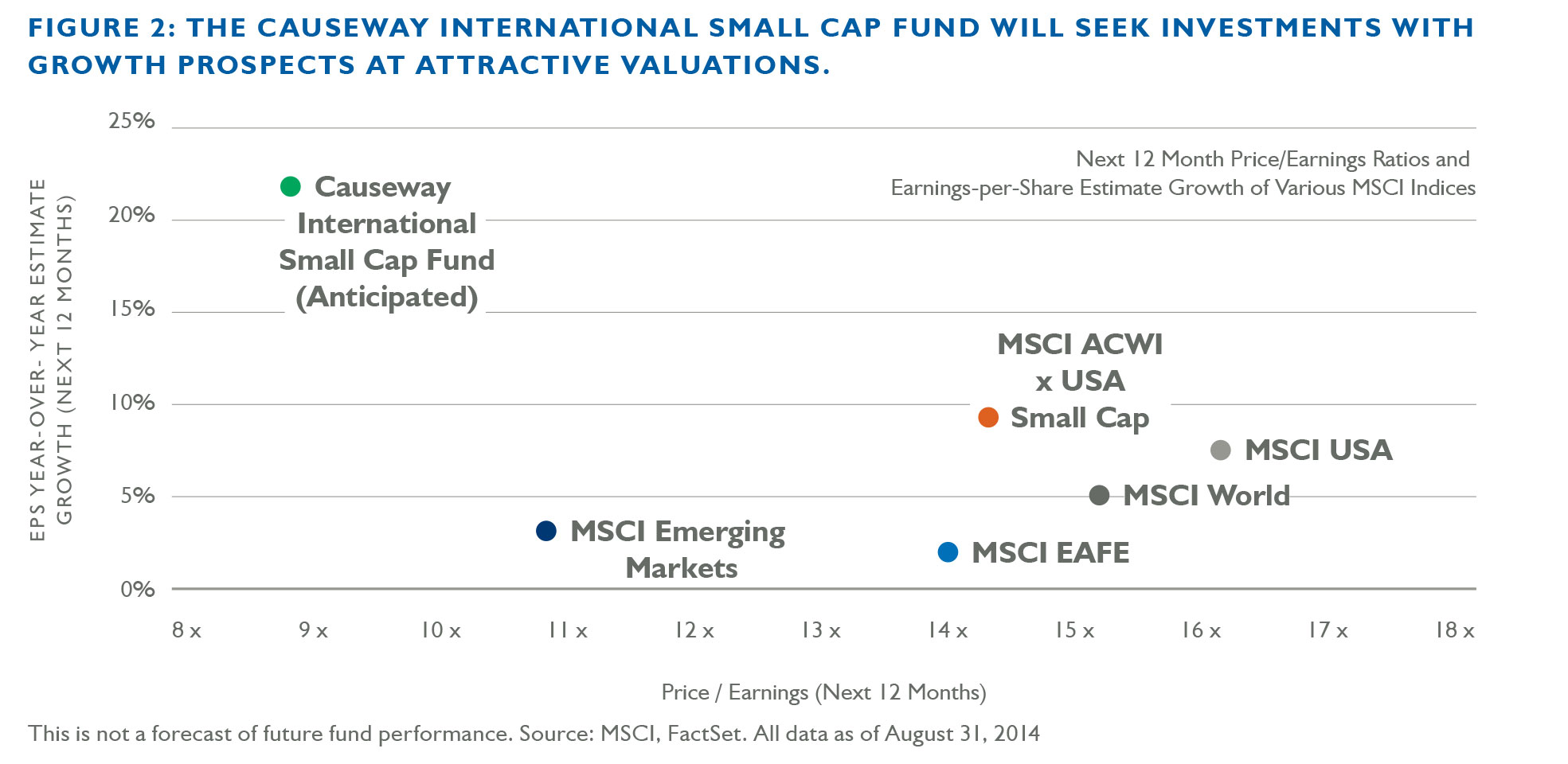

Relative to the ACWI ex-US Small Cap Index, we anticipate positioning the Causeway International Small Cap portfolio to combine better growth potential with a meaningful valuation discount.

Why invest in small caps now, in the wake of such a prolonged equity bull market?

DK: We believe international small cap stocks currently offer higher growth compared with their larger peers, while trading in line with global benchmarks from a valuation perspective. The weighted average expected next-twelve-month (NTM) earnings-per-share (EPS) growth rate for ACWI ex-US Small Cap Index constituents is 9%, nearly double the rate of the MSCI World Index and five times that of the MSCI EAFE Index, with its large exposure to Europe. Meanwhile, valuation of the companies in the ACWI ex-US Small Cap Index is still reasonable at a price-to-earnings ratio of 14.3x NTM earnings. Relative to the ACWI ex-US Small Cap Index, we anticipate positioning the Causeway International Small Cap portfolio to combine better growth potential with a meaningful valuation discount.

Arjun, why does it make sense to use a quantitative strategy to select small cap stocks?

AJ: Either a fundamental or a quantitative approach can work effectively in the world of small cap stocks. Each approach has its own advantages and drawbacks. We believe that the major advantages of quantitative analysis are its rapid assessment of multiple alpha sources and its risk management capabilities. Fundamental research is a time-intensive process, and a large fundamental research team would be required to effectively cover the thousands of stocks in our investment universe. Fundamental in-depth research is more easily allocated to fewer, larger stocks that can absorb more investment dollars. We believe that our quantitative tools allow us to screen for minimum liquidity thresholds, model the expected market impact from a new position, and incor-porate this directly into our net estimate for expected alpha. In our view, these extra liquidity inputs are essential for small cap stocks.

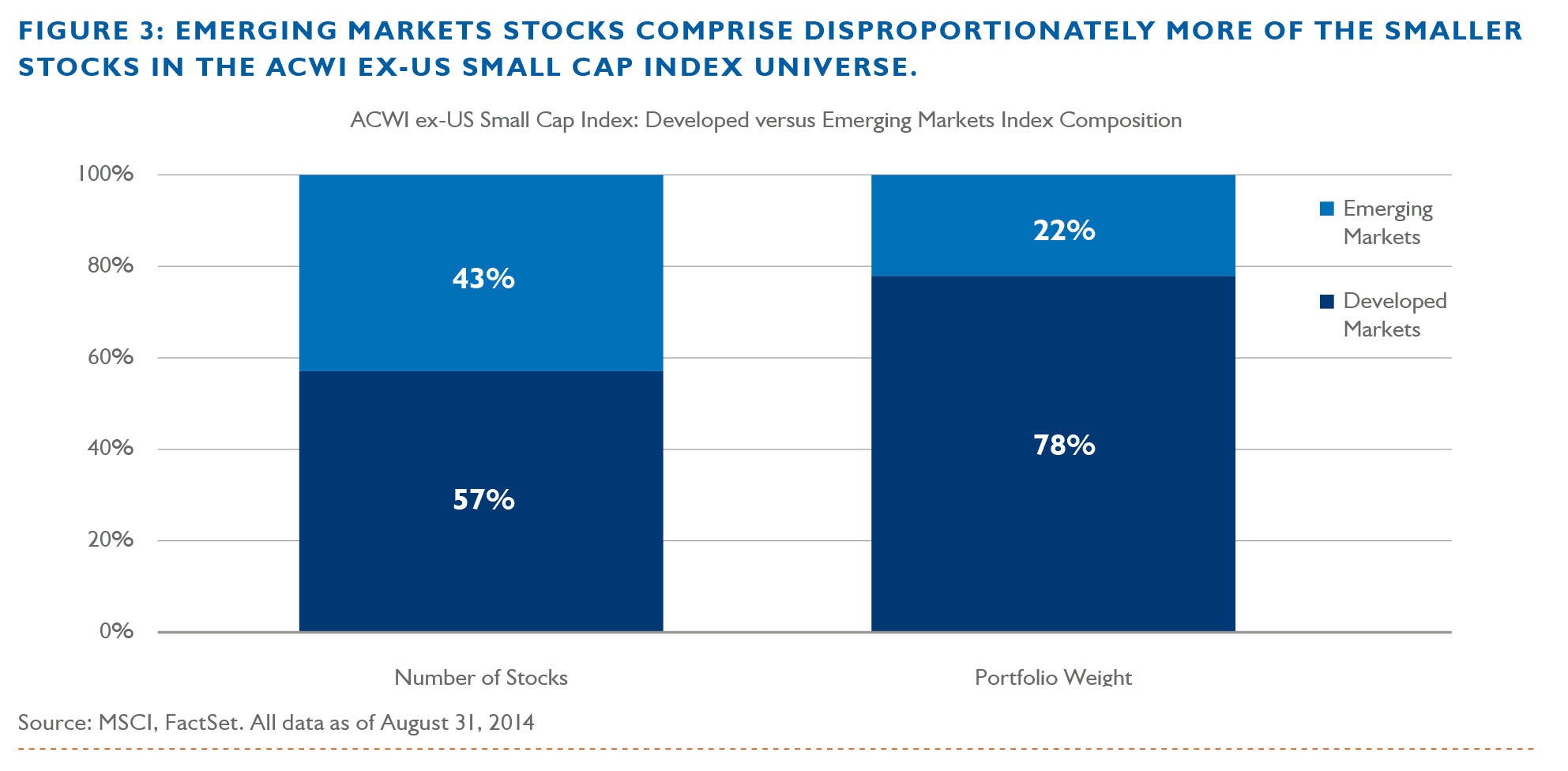

JG: A disproportionate number of small cap stocks also reside in emerging markets, and we believe that our experience investing in these markets over the past seven years gives us an advantage. While stocks based in emerging markets represent only 22% of the weight in the ACWI ex-US Small Cap Index, these emerging markets stocks represent 43% of the constituent names. We believe that a quantitative process allows more efficient access to emerging markets small cap stocks, which may include some of the most lucrative sources of alpha in the ACWI ex-US Small Cap Index.

How does your investment process seek to exploit opportunities in the small cap equity universe?

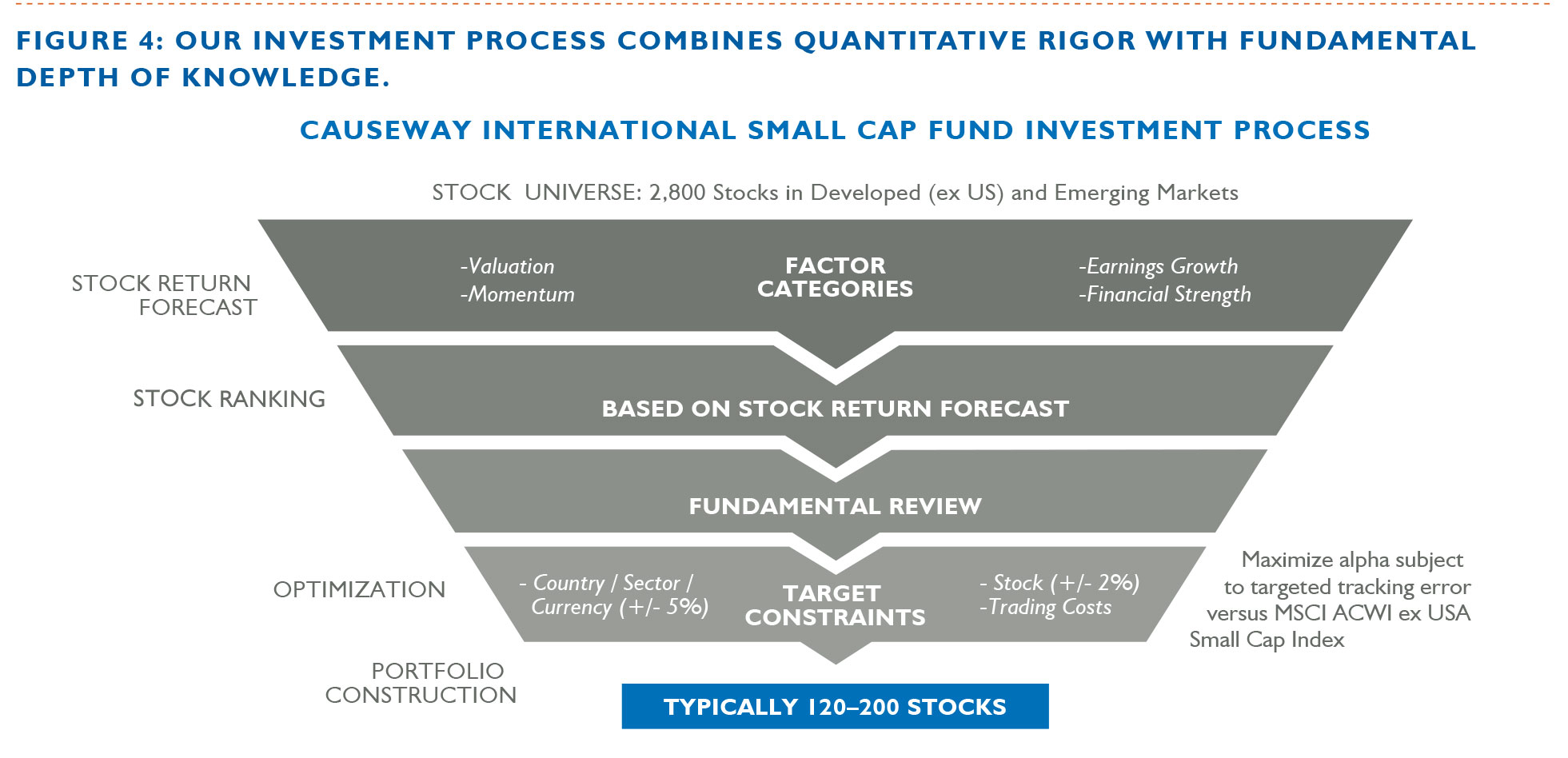

AJ: We examine a multitude of factors within four main categories to gauge the return potential of a stock. First, we seek relatively inexpensive valuations. Second, we want to see accelerating earnings growth prospects and upward earnings estimate revisions from the sell-side analysts who cover the stock. Third, we want to see positive recent momentum, since recent trends tend to persist. And fourth, we want to find financial strength by seeking stocks with a focus on strong free cash flow generation rather than simply sales growth. We then rank the stocks on these factors to identify candidates that will produce the most attractive risk-adjusted returns. Additionally, as with our other quantitatively-managed strategies at Causeway, we believe that fundamental input can strengthen our portfolio and further reduce risk. Before we establish new positions, our fundamental portfolio managers and analysts review stocks in their sector of coverage and report any “red flags” that may be outside the scope of quantitative analysis. For instance, our fundamental analysts may identify significant corporate actions or management changes, or be aware of pending regulatory changes, litigation risk, merger and acquisition activity, or off-balance sheet liabilities that may be difficult to anticipate or detect with a purely quantitative approach.

Small caps may have impressive return potential, but they also bring significant risk. How do you control for risk in individual stocks as well as for overall portfolio volatility?

AJ: It’s true that, in general, greater potential returns come with greater expected volatility. We take many steps to monitor and manage risk within the portfolio. We start by including in our tradable universe only the roughly 2,800 stocks that trade at least $1 million per day on average, to ensure sufficient liquidity and to minimize market impact when we enter and exit positions. We intend for our portfolio to also typically contain between 120 and 200 stocks at any one time, and this breadth is intended to limit idiosyncratic risk. Additionally, we seek to have a maximum active exposure – meaning portfolio exposure relative to the ACWI ex-US Small Cap Index – of 2% to any single stock at the time of rebalance (creating an effective maximum position size of 2.3% using current index weights). We use this to help constrain the impact of rapid moves in individual holdings.

Not only does our process seek stocks with high expected returns, but it also favors stocks that will help offset existing risks in current holdings and lower overall portfolio volatility.

JG: Causeway’s proprietary multifactor risk model also provides us with detail to assist with risk analysis and risk management. When we optimize our portfolio, we seek to maximize risk-adjusted return with our risk model, which examines over 80 different components to assess the marginal risk that a new position will add. We have 13 years of experience applying various aspects of our proprietary risk model to global equities, and benefit from being able to “look under the hood,” so to speak, to understand the output and refine the factors. Not only does our process seek stocks with high expected returns, but it also favors stocks that will help offset existing risks in current holdings and lower overall portfolio volatility. Lastly, our fundamental review serves an important role in managing “tail risk” in individual positions.

Joe, dedicated small capitalization investing is a new area for Causeway. Why do you think Causeway’s experience will transfer easily to smaller stocks?

JG: While this is Causeway’s first small-cap fund, we are definitely not new to small-cap investing. Causeway Emerging Markets Fund, which launched in 2007, is also quantitatively managed. Within that strategy, we frequently encounter smaller cap companies with below-average levels of liquidity. And as we previously mentioned, emerging market stocks compose 43% of the stocks in our small cap universe. With a seven-year track record of managing our Emerging Markets Fund, we have developed considerable experience with many of the same proven alpha forecasting factors that we expect will carry over to the International Small Cap Fund.

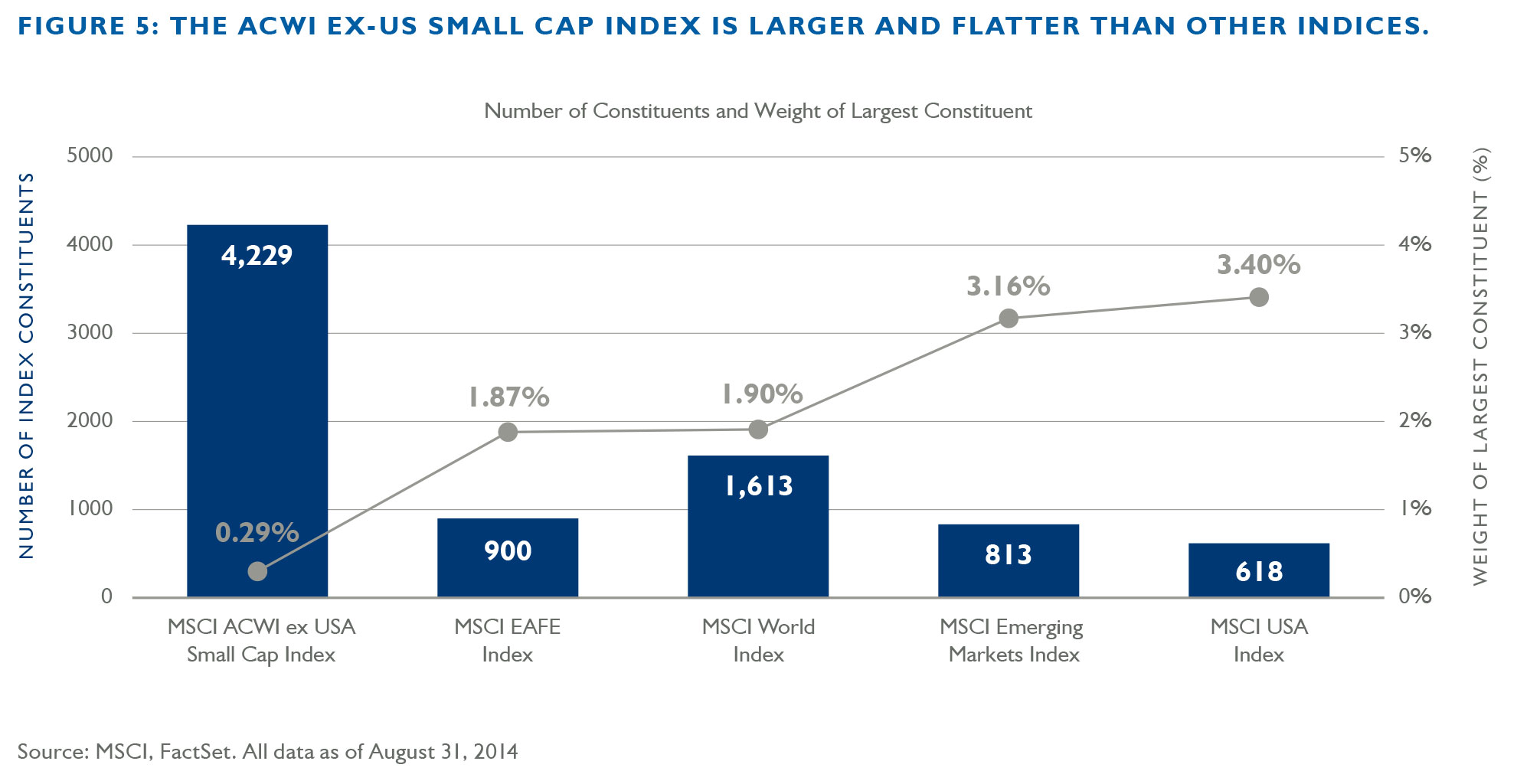

Duff, your investable universe is the ACWI ex-US Small Cap Index. What kind of opportunity set does this provide?

DK: In contrast to some of the major world equity indices, the ACWI ex-US Small Cap Index has many more constituents, currently over 4,200, with roughly equal weightings. This creates an index with similar position sizing (the largest constituent currently represents only 0.29% of the ACWI ex-US Small Cap Index), versus more concentrated positions in the larger-cap indices, such as MSCI World and MSCI EAFE. We believe that this flat composition will provide us with access to under-valued, up-and-coming companies across many industries in 45 countries, both developed and emerging.

AJ: The large number of constituents and similar position sizing make it very challenging to replicate the ACWI ex-US Small Cap Index on a passive basis. In many cases, exchange-traded funds (ETFs) that track the international small cap segment of the markets have significant annual tracking errors versus the ACWI ex-US Small Cap Index. If an investor accepts these levels of tracking error, we believe that they should reject the ETFs and attempt to capture the higher excess returns (alpha) that active management can provide.

DK: We are excited to find another opportunity to combine the flexibility and breadth of quantitative analysis with Causeway’s wealth of global industry knowledge. We believe that this collaboration has already proven its worth in emerging markets.

Important Disclosures

Causeway Capital Management LLC, the investment adviser, manages international, global, and emerging markets equity assets for corporations, pension plans, public retirement plans, sovereign wealth funds, superannuation funds, Taft-Hartley pension plans, endowments and foundations, mutual funds, charities, private trusts and funds, wrap fee programs, and other institutions. Mutual fund investing involves risk, including possible loss of principal. In addition to the normal risks associated with equity investing, international investing may involve risk of capital loss from unfavorable fluctuations in currency values, from differences in generally accepted accounting principles, or from economic or political instability in other nations. Emerging markets involve heightened risks related to the same factors, as well as increased volatility and

lower trading volume. Investments in smaller companies involve additional risks and typically exhibit higher volatility.

This information must be preceded or accompanied by the current prospectus for Causeway International Value Fund, Causeway Global Value Fund, Causeway International Opportunities Fund, Causeway Emerging Markets Fund, Causeway Global Absolute Return Fund and Causeway International Small Cap Fund. Please read the summary or full prospectus carefully before you invest or send money. To obtain additional information including charges, expenses, investment objectives, or risk factors, or to open an account, call 1.866.947.7000, or visit us online at www.causewayfunds.com.

Causeway Capital Management LLC serves as investment adviser for each Fund. The Funds are distributed by SEI Investments Distribution Co., 1 Freedom Valley Dr., Oaks, PA, 19546, which is not affiliated with Causeway Capital Management LLC.

Market Commentary

The views expressed above and portfolio characteristics are subject to change. Any portfolio characteristics for Causeway International Small Cap Fund are based on the portfolio managers’ expectations for that Fund as of the date hereof, and may not reflect the actual characteristics of the Fund at launch or in the future. There is no guarantee that any forecasts made will come to pass. Any portfolio securities identified and described do not represent all of the securities purchased, sold, or recommended for client accounts. The reader should not assume that an investment in the securities identified, if any, was or will be profitable. “Alpha” is a measurement of performance return in excess of a benchmark index. “Tracking Error” is the volatility of alpha over the stated preceding period. A “Weighted Average” measures a characteristic by the market capitalization of each stock. “Earnings-per-Share” is the portion of a company’s profit allocated to each outstanding share of common stock.

Index Disclosures

The MSCI ACWI ex USA Small Cap Index captures small cap representation across 22 of 23 developed markets (excluding the US) and 23 emerging markets. With 4,229 constituents, the index covers approximately 14% of the global equity opportunity set outside the US. The MSCI EAFE Index is a free float-adjusted market capitalization weighted index, designed to measure developed market equity performance excluding the U.S. and Canada, consisting of 21 stock markets in Europe, Australasia, and the Far East. The MSCI World Index is a free float-adjusted market capitalization weighted index, designed to measure developed market equity performance, consisting of 23 developed country indices, including the U.S. The MSCI Emerging Markets Index is a free float-adjusted market capitalization index, designed to measure equity market performance of emerging markets, consisting of 23 emerging country indices. The MSCI All Country World Index ex U.S. is a free float adjusted market capitalization weighted index, designed to measure the equity market performance of developed and emerging markets excluding the U.S. The MSCI USA Index is a free float-adjusted market capitalization weighted index, designed to measure large- and mid-cap US equity market performance. The MSCI USA Index is member of the MSCI Global Equity Indices and represents the US equity portion of the global benchmark MSCI ACWI Index. The Indices are gross of withholding taxes, assume reinvestment of dividends and capital gains, and assume no management, custody, transaction or other expenses. It is not possible to invest directly in these indices. The Funds may invest in countries not included in their benchmark indices. MSCI has not approved, reviewed or produced this report, makes no express or implied warranties or representations and is not liable whatsoever for any data in the report. You may not redistribute the MSCI data or use it as a basis for other indices or investment products.