Contact Us

Subscribe to Causeway Insights, delivered to your inbox.

When Causeway first launched global value equity over 12 years ago, we did not fully anticipate the potential of investing in global versus international developed markets. Although more efficient, on average, than its foreign peers, the US equity market invariably offers opportunities to exploit mispricing. The breadth and depth of the US equity market lends itself well to a developed markets portfolio without geographic limits.

“When a man has put a limit on what he will do, he has put a limit on what he can do.” – Charles M. Schwab

From Causeway’s inception in 2001, we embraced global equity as an alternative to the constrained international equity mandates requested by the vast majority of our clients. We recognized the benefits of screening globally for undervaluation among the world’s best-run companies. The developed global investable universe is comprised of over twice the number of companies in the developed international universe. As a result, global has the potential to deliver significant performance advantages versus international. However, when we first launched global value equity over 12 years ago, we did not fully anticipate the potential of investing in global versus international developed markets. Although more efficient, on average, than its foreign peers, the US equity market invariably offers opportunities to exploit mispricing. The breadth and depth of the US equity market lends itself well to a developed markets portfolio without geographic limits. Unlike a dedicated US equity portfolio, a global portfolio may hold varying amounts of US-listed stocks. From a bottom-up perspective, we compare the risk-adjusted total return potential of the US-listed stocks to non-US alternatives. If given the choice, we prefer global equity mandates over international for their flexibility and their greater number of potential investment candidates. The arguments for separating US and non-US equities typically revolve around a misguided notion of diversification. Today, many US-domiciled investors still think of their US equities as “core,” and international equities as something different, unrelated to the US market. We argue just the opposite. High (and increasing) correlations of US and non-US equity returns imply that global factors eclipse local factors in driving developed market returns. Over the past 20 years, we have observed that industry-specific valuation differences in the developed markets have narrowed– and often vanished – across borders. Multi-national and/or exporting companies in the same industry, regardless of geographic domicile, share similar opportunities for growth.

The arguments for separating US and non-US equities typically revolve around a misguided notion of diversification.

Efforts by investors to partition US from non-US developed markets also stemmed from a notion of specialization. How could an expert in non-US developed markets also succeed in the US market – and vice versa? Yet, we note, if research analysts do not span the globe, how can they ever understand fully their industries and the competitive environment? We believe that our analysis must compare political, regulatory and social changes impacting companies in one country/region, and weigh the possible contagions to other regions. To explore this comparison of global versus international, we spoke to Causeway fundamental and quantitative portfolio managers, Jamie Doyle and Joe Gubler.

Jamie and Joe, what evidence do you have in favor of giving an asset manager geographic discretion?

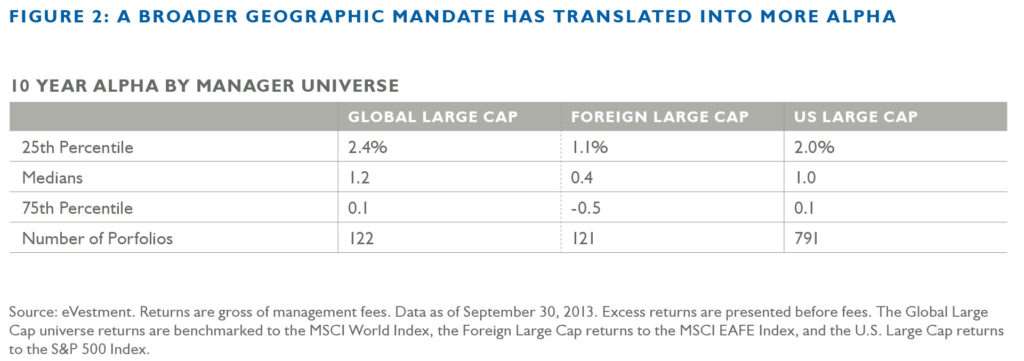

JD: I always start with Causeway’s own track record. Our global value equity strategy has delivered an annualized 12%, net of fees, and returned 4.5% in excess of the MSCI World Index (to 12/31/13). This compares favorably with Causeway’s international value equity strategy, which does not invest in the US, with an average annual return since inception of 9.4% and alpha of 3.1% versus the MSCI EAFE Index. For a bigger picture, we compared a universe of global portfolios to their international and US peers. The comparison corroborated our own positive experience with global equity.

As the diversification benefit of investing across developed markets diminishes, it becomes more important for managers to make intelligent risk/return tradeoffs within the portfolio across other dimensions of risk.

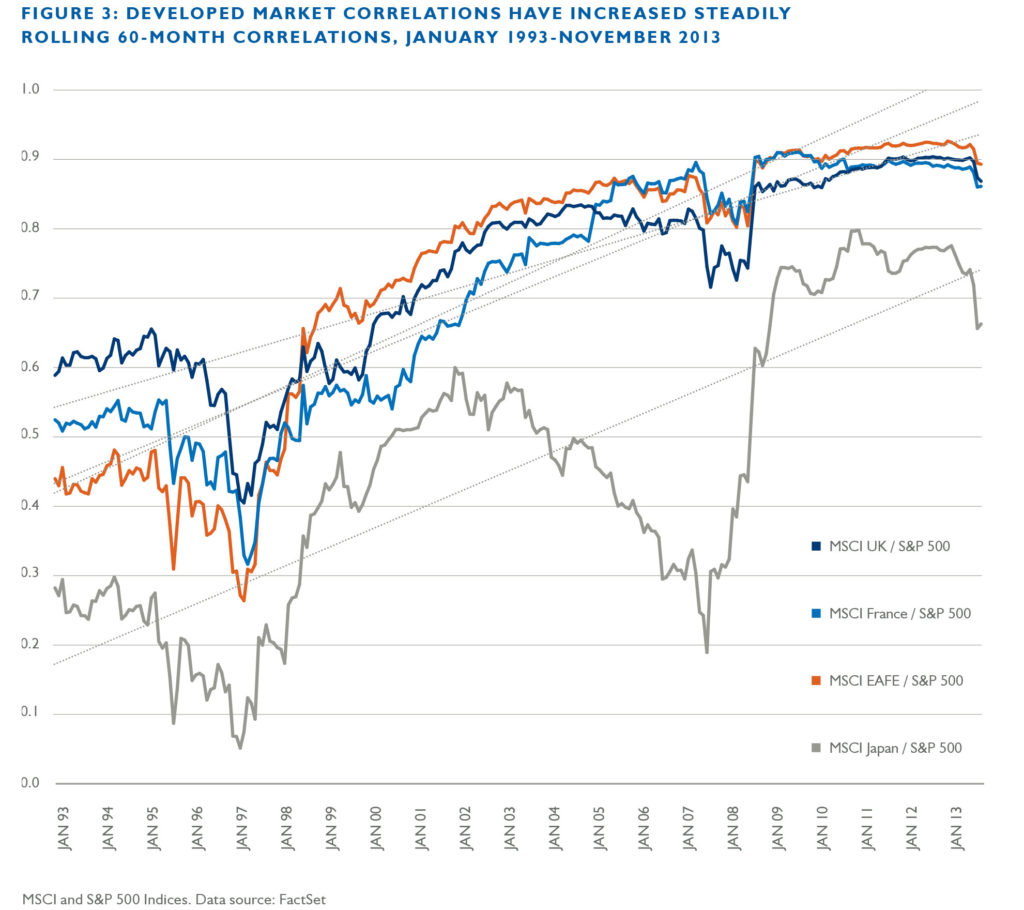

JG: As for the benefit of separating non-US and US equity exposures to reduce volatility, only the Japanese market still appears to provide some element of diversification in a rolling 60 month analysis. If we shorten the regression to the past decade and past five years, we see that benefit of adding Japanese stocks eroding. As the diversification benefit of investing across developed markets diminishes, it becomes more important for managers to make intelligent risk/return tradeoffs within the portfolio across other dimensions of risk. A manager with a single global mandate has more flexibility to do this than multiple managers with separate US and non-US portfolios.

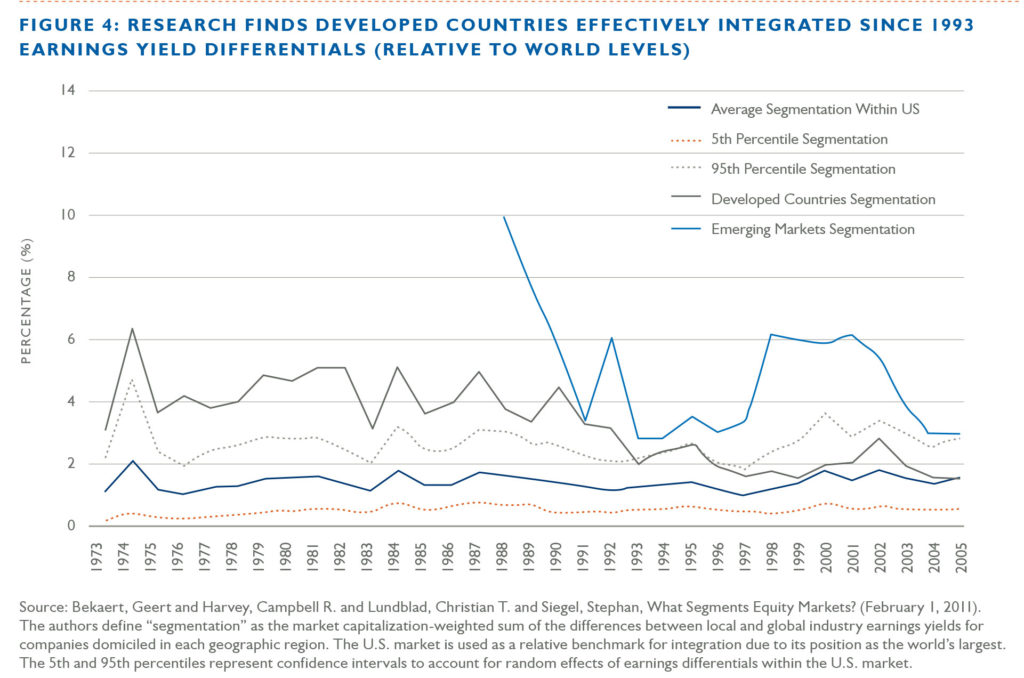

JD: For our clients who want maximum equity diversification, we can also combine our global developed markets equity with our emerging markets strategy (what we call the Causeway global opportunities strategy), benchmarked to an all-country benchmark, such as the MSCI All Country World Index (ACWI). In a 2011 paper by Bekaert et al, the authors reveal the convergence of earnings yields of stocks in developed countries relative to the yield of the MSCI World Index from the early 1970s to 2005. Emerging markets, however, have not exhibited the same integration, and they continue to offer diversification benefits versus developed markets.

Over time, we expect that many of our clients will desire the benefits of a geographically limitless portfolio, one that takes full advantage of all of Causeway’s detailed research and experienced stock selection.

Jamie, how can clients understand their portfolios’ geographic exposures?

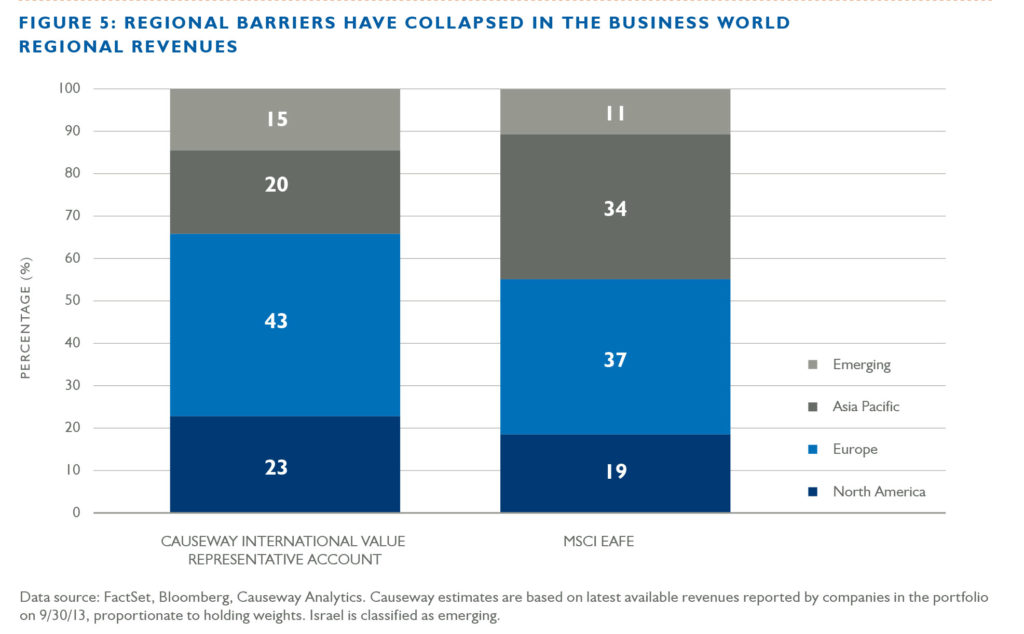

JD: Causeway uses a proprietary multi-factor risk model to help our fundamental portfolio managers use diversification as a tool to lower prospective volatility of returns. However, few clients want to dive into the statistics and evaluate the region and currency factors in our model. As an alternative, we provide clients with the revenue breakdown of the companies that comprise their international and global portfolios. It might be surprising for clients to realize that their “international” portfolio is filled with companies generating 23% of sales in North America and 15% in emerging markets. Even though the EAFE Index appears somewhat similar in revenue split, this revelation can be disquieting for clients who place their equities in geographic silos.

Confidence in our global research allows us to concentrate the number of stocks in our global portfolios. With such a large investable universe, global provides the potential to achieve lower levels of volatility than in international equity. As a research team, we are not surprised by the borderless nature of many companies. The better-managed companies will continue to expand wherever they can benefit their shareholders. In response to this corporate diaspora, we must continue to measure our portfolio’s ever-changing geographic risk. Over time, we expect that many of our clients will desire the benefits of a geographically limitless portfolio, one that takes full advantage of all of Causeway’s detailed research and experienced stock selection – and one that does not restrict us to less than half of the developed markets universe. US versus non-US segmentation can constrain performance and may not achieve the diversification goal. As for a New Year’s resolution, we suggest, “Go Global.”

Important Disclosures

The Firm, Causeway Capital Management LLC (“Causeway”), is organized as a Delaware limited liability company and began operations in June 2001. It is registered as an investment adviser with the U.S. Securities and Exchange Commission under the Investment Advisers Act of 1940. Causeway manages international, global, and emerging markets equity assets for corporations, pension plans, public retirement plans, Taft-Hartley pension plans, endowments and foundations, mutual funds, charities, private trusts and funds, wrap fee programs, and other institutions. The firm includes all discretionary and non-discretionary accounts managed by Causeway.

Causeway claims compliance with the Global Investment Performance Standards (GIPS®).

The International Value Equity Composite (“International Composite”) includes all U.S. dollar denominated, discretionary accounts in the international value equity strategy, which do not apply a minimum market capitalization requirement of $2.5 billion or higher ($5 billion or higher prior to November 2008), permit investments in South Korean companies after October 2003, do not regularly experience daily external cash flows, and are not constrained by socially responsible investment restrictions. The international value equity strategy seeks long-term growth of capital and income through investment primarily in equity securities of companies in developed countries located outside the U.S. From June 2001 through November 2001, the International Composite included a non-fee-paying account with total assets of approximately $2 million. This was the sole account in the International Composite from June through September 2001. The account was included in the International Composite at account inception because it was fully invested at inception. The benchmark is the MSCI EAFE Index.

The Global Value Equity Composite (“Global Composite”) includes all U.S. dollar denominated, discretionary accounts in the global value equity strategy which are not constrained by socially responsible investment restrictions. Through March 30, 2007, Causeway managed the Global Composite using research and recommendations regarding U.S. value stocks from an unaffiliated investment advisory firm under a research services agreement for an asset-based fee. The global value equity strategy seeks long-term growth of capital and income through investment primarily in equity securities of companies in developed countries located outside the U.S. and of companies located in the U.S. The benchmark is the MSCI World Index.

New accounts are included in the Composites after the first full month under management, except as noted for the International Composite above. Terminated accounts are included in the Composites through the last full month under management. Account returns are calculated daily. Monthly account returns are calculated by geometrically linking the daily returns. The returns of the Composites are calculated monthly by weighting monthly account returns by the beginning market values. Valuations and returns are computed and stated in U.S. dollars. Returns include the reinvestment of interest, dividends, and any capital gains. Returns are calculated gross of withholding taxes on dividends, interest income, and capital gains. The firm’s policies for valuing portfolios, calculating performance, and comparing compliant presentations are available upon request. Gross-of-fees returns are presented before management, performance-based and custody fees, but after trading expenses. Net-of-fees returns are presented after the deduction of actual management fees, performance-based fees and all trading expenses, but before custody fees. Causeway’s basic management fee schedules are described in its firm brochure pursuant to Part 2 of Form ADV.

Past performance is no guarantee of future performance. In addition to the normal risks associated with investing, international investments may involve risk of capital loss from unfavorable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Emerging markets involve heightened risks related to the same factors as well as increased volatility and lower trading volume.

The MSCI EAFE Index is an arithmetical average weighted by market value of the performance of approximately 1,000 non-U.S. companies representing 22 stock markets in Europe, Australasia, New Zealand and the Far East. The MSCI World Index is a free float-adjusted market capitalization index, designed to measure developed market equity performance, consisting of 24 developed country indexes, including the U.S. It is not possible to invest directly in these indices. Accounts in the Composites may invest in countries not included in their benchmark indices.

MSCI has not approved, reviewed or produced this report, makes no express or implied warranties or representations and is not liable whatsoever for any data in the report. You may not redistribute the MSCI data or use it as a basis for other indices or investment products.

Contact Sarah Van Ness at 310-231-6127 or [email protected] to request a complete list and description of firm composites and/or a presentation that adheres to the GIPS® standards.

Market Commentary

The market commentary expresses the portfolio managers’ views as of 12/31/2013 and should not be relied on as research or investment advice regarding any stock. These views and portfolio holdings and characteristics are subject to change. There is no guarantee that any forecasts made will come to pass. Any portfolio securities identified and described do not represent all of the securities purchased, sold, or recommended for client accounts. The reader should not assume that an investment in the securities identified was or will be profitable.